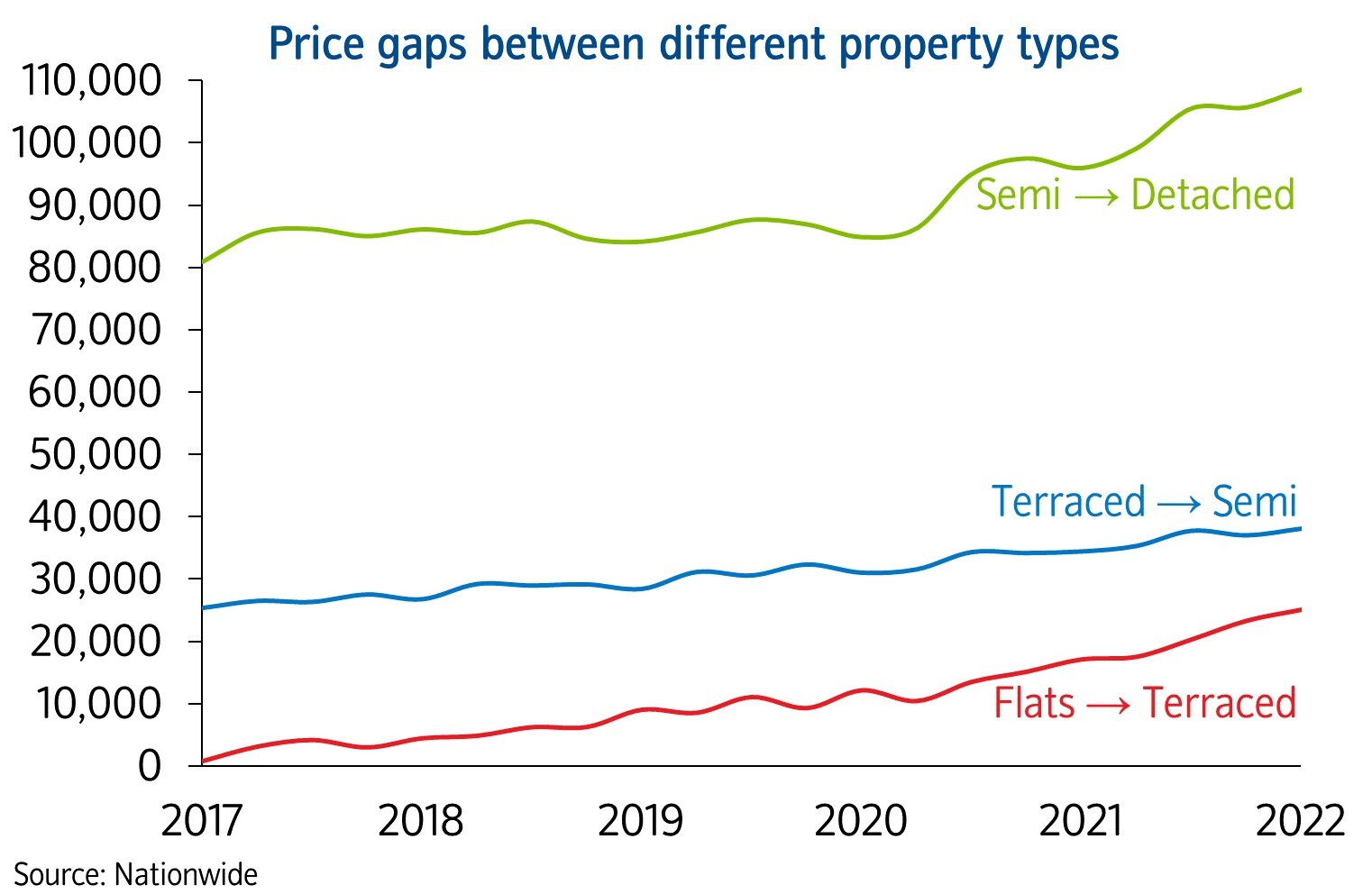

Despite all the external geopolitical news & fear over a flattening yield curve, the UK residential property market continues to go from strength to strength, with house prices rising 14.3% YoY in March accordingly to Nationwide Building Society (see charts).

Sure this might cool off later in 2022, as inflation further bites into consumers’ wallets.

Yet equally, the RMI sector remains robust thanks to the need to upgrade ageing properties (re decarbonisation) & the shift towards premiumisation, alongside the government’s pledge to construct 300,000 new homes annually (vs c. 200k today), ‘Build to Rent’, recladding & greater infrastructure spend (eg HS2, nuclear).

All in all providing a favourable backdrop for Lords Group Trading. A rapidly expanding, specialist UK builders merchant (51% of EBITDA) and heating/plumbing (49%) distributor, addressing a £55bn TAM (+5% pa).

80% of its revenues are derived from RMI, with the vast majority coming from local tradesmen, hardware stores, plumbing/heating merchants & construction companies (ie B2B).

All underpinned by excellent customer service, in-house technical expertise, next day delivery & an up-to-the minute order tracking solution (ie benefits client site planning).

Today the group announced two synergistic ‘bolt-on’ acquisitions – both of which I believe will be earnings enhancing & importantly value accretive.

Namely, the purchase of DH&P Plumbing & Heating for £9.3m ( equivalent to 4.7x trailing EV/EBITDA) and Hevey Building Supplies for £2.2m (4.4x EBITDA).

The former adding to LORD’s already rapidly expanding & popular ‘Mr Central Heating’ brand, with the 2nd filling out the group’s building products footprint in the East of England.

So what does this mean wrt the numbers?

Well personally I’ve upgraded my FY22 sales, EBITDA & EPS (+6%) forecasts to £444m, £26.6m & 7.7p/share respectively. Ending the period with net debt of £43m, on top of EPS climbing 10% to 8.8p in FY23.

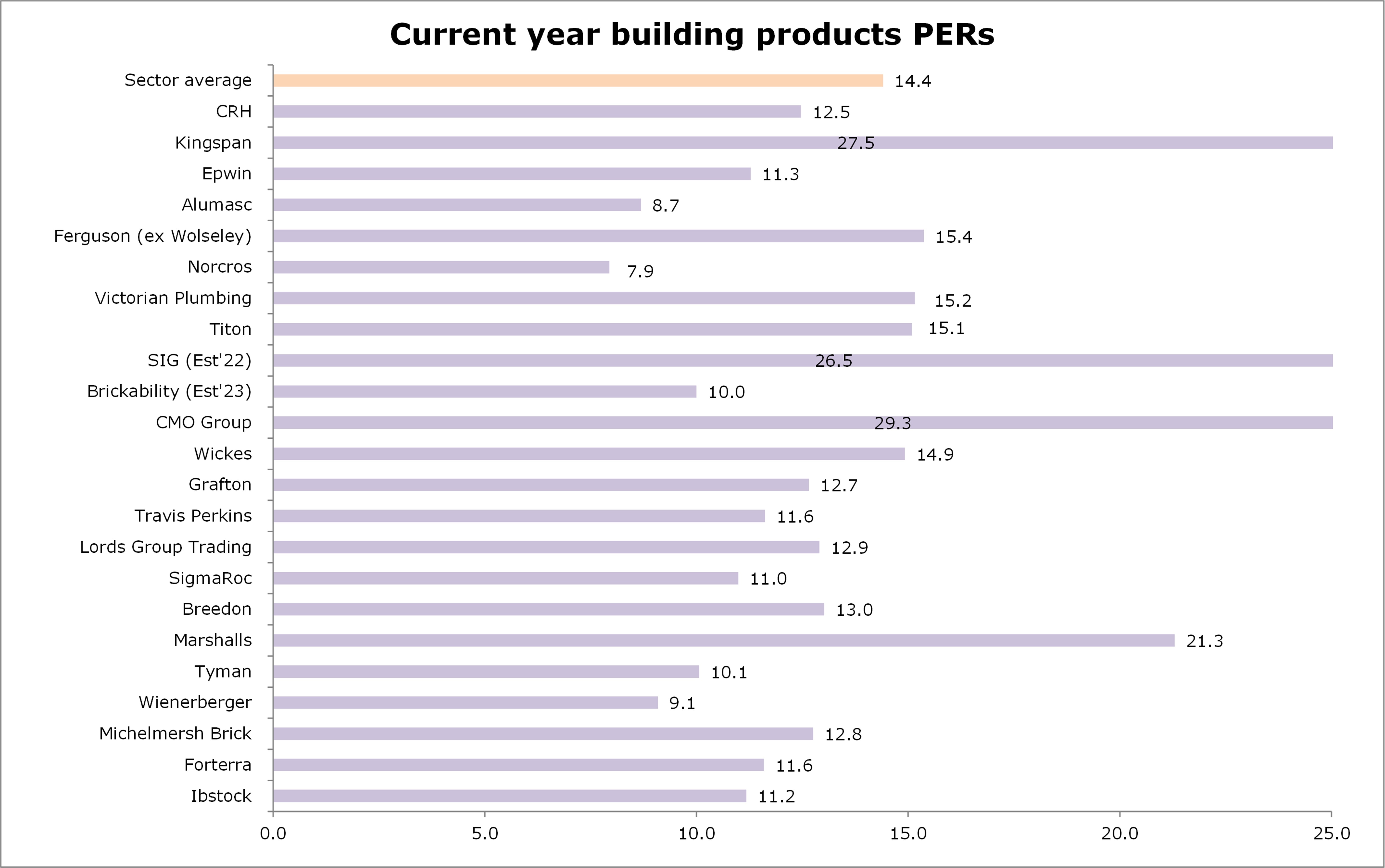

Hence at 100p, the stock trades on modest CY EV/EBITDA and PE multiples of 7.5x & 12.9x. Whereas from a valuation perspective, I would rate the stock on a 15x FY’23 PER, equivalent to c. 132p/share.

CEO Shanker Patel adding: " DH&P will be highly complementary to our existing Mr Central Heating and APP Wholesale businesses." Whilst "Hevey will further enhance our presence in the East of England".