Broker Greenwood Capital says Rift Helium’s (RIFT ) Rukwa project could be generating US$63 million per year from its assets in Tanzania from 2031.

The broker sets a risked valuation and near term target for Rift of 32p per share.

In a long and in-depth note the broker laid out various development scenarios for Rift’s Rukwa project, and using a series of assumptions presented a detailed model of a possible financial future for the company.

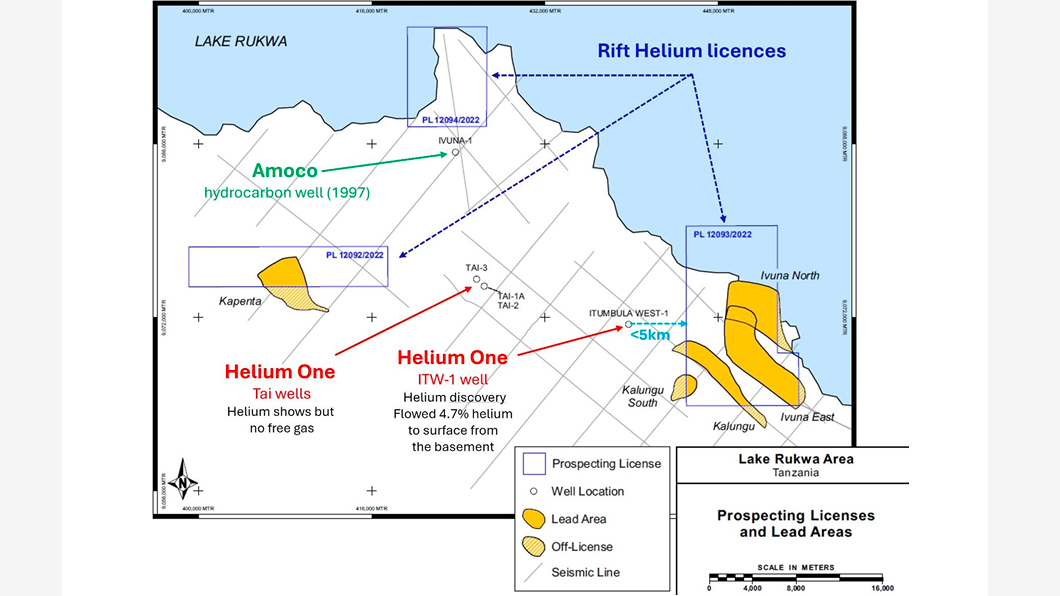

Rift plans to shoot seismic in Tanzania this year, and then move to drilling in 2027.

Production should follow fairly rapidly thereafter.

Greenwood modelled a 200 million cubic feet per year helium operation, selling at US$500 per thousand cubic feet of helium.

By 2030, Greenwood reckons free cash will run at US$2 million.

But it’s in 2031 that the model really shows the potential of the Rukwa assets.

From 2031 to 2033 the assets look set to generate US$63 million per year, according to Greenwood. That then drops to US$60 million in 2034, and US$57 million from 2035 to 2039.

Taken in total, these are some pretty big numbers for a company that’s only capitalised at around £10 million.

“Under our US$500/mcf base-case, annual gross revenue averages US$88 million over the life of the operation, annual EBITDA averages US$73 million and free cash averages US$43 million per year with average free cash flow at steady-state production being US$50 million per year demonstrating the project has the potential for rapid payback,” said Greenwood.

“This assumes total helium production over the life of project of 2.8bcf which is note is only a small part of Rift’s large 2U P50 19.1 billion cubic feet prospective helium volume. Clear upside remains if higher flow rates are achieved or a larger well development is established. Given the anticipated low complexity of the expected gas flow (no hydrocarbons) and proven nature of helium separation technology, a long ramp-up period is likely not required and we believe that nameplate could potentially be reached soon after commissioning is complete.

View from Vox

Lots of upside presented here by Greenwood, which also talks elsewhere in the note in some detail about the ongoing supply disruptions in the wider helium market. Could it be that Greenwood’s pricing assumptions turn out to be conservative? Given that production from Qatar and Russia has been severely disrupted in recent weeks the answer to that question is likely to be ‘yes’. There’s also the question of just how much helium Rift actually has. Greenwood here models a sensible production scenario based on a reasonably cautious assessment of the potential helium resource base at Rukwa. The seismic due to be shot this year should tell us a lot more about whether the estimates as they currently stand are reasonably, or whether, as might be the case, they undershoot. But even allowing for the broker’s understandable caution, the scenarios that are presented make for compelling reading. It will certainly be an interesting year or two for Rift from here on in.