Avacta - Developing truly innovative new drugs & diagnostics can take years.

Albeit from today’s positive & ‘on track’ H1’22 results, Avacta AVCT seems to be successfully doing this on numerous fronts & at double quick time.

Financial Highlights

In terms of the H1 numbers, net cash (ex IFRS16) closed June at a healthy £17m & is forecast by Stifel to be £8.5m by Dec.

CEO Alastair Smith commenting: "The Phase I clinical trial evaluating the safety & tolerability of AVA6000 is making excellent progress."

"I believe success [here would] be a major value inflection point. As, not only is it important for the continued development of AVA6000, but it will also provide validation of the pre|CISION mechanism of action, and therefore the platform as a whole. If then applied more broadly, the validated platform would create a promising pipeline of chemotherapies with the potential to significantly improve patients' lives."

"Our Diagnostic Division is now focused on developing a pipeline of IVD products outside of Covid19, that will underpin a future profitable IVD business”.

View from Vox

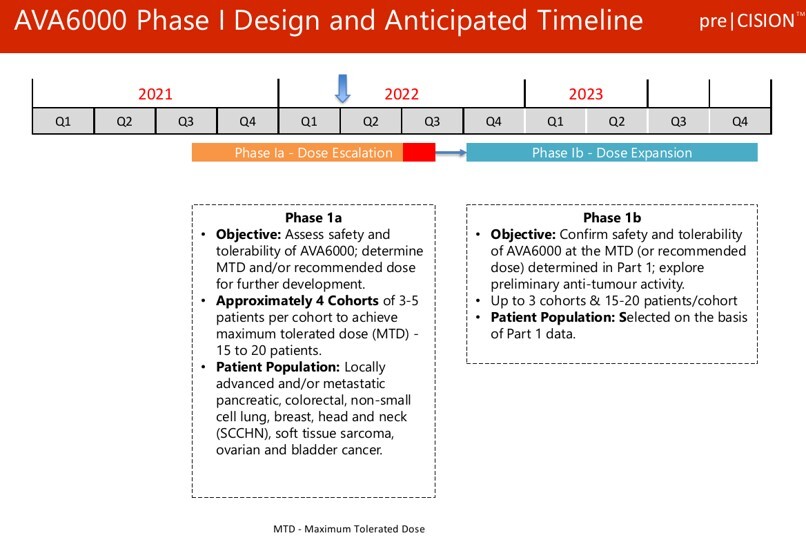

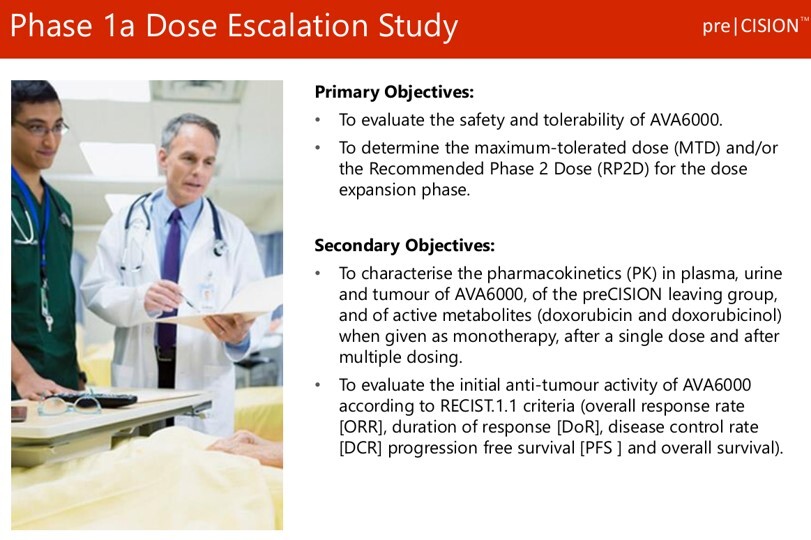

To us, the most important near term ‘value catalyst’ is the continued Phase 1 clinical trial of pro-doxorubicin (AVA6000), that recently advanced to the 4th patient cohort at a dosage (200mg/m2) of >2x the usual prescribed level.

Saying to me, that the safety & tolerability of this potentially ground-breaking therapeutic appears to be fine, even for seriously ill people. Caveated of course, that the study is still ongoing & this is my own opinion, as a non-medic.

Nonetheless, to get so far so quickly is a testament to AVCT’s ambitions & capability. Particularly, given the US FDA also granted AVA6000 Orphan Drug Designation (ODD) for the rare disease of soft tissue sarcoma (<1% of adult tumours) in early Sept. Further rubber stamping the quality of the science, alongside the prodrug’s applicability & safety profile.

1st results from Phase 1a of the trial are scheduled for Q4’22, which hopefully should also include pharmacokinetics (PK) data. Alongside providing some important ‘mechanical’ info from tumour biopsies to see whether the chemo-payload is being deposited (re FAPα-activated) & absorbed by the cancerous cells.

Assuming this is the case, then IMO it would be a terrific endorsement of both AVA6000 & the wider pre|CISION platform. Implying a much higher probability of achieving a significantly improved efficacy than simply using doxorubicin on its own.

Why? Well, in its raw form doxorubicin is one of the most powerful chemotherapies ever invented. Its been used for years & has been medically proven to shrink/destroy tumours. The main problem is that it harms healthy tissues, especially around the heart - & so typically is used in only small doses & for limited periods.

Nevertheless regardless of the final outcome, Avacta has plenty of other opportunities too. Not least its next candidate AVA3996 (Velcade analogue) which is progressing towards an IND filing in 2023 & its radiopharmaceuticals partnership with POINT Biopharma.

Elsewhere, the Affimer platform is making great strides too, both in terms of drug discovery (eg bispecifics, TMAC, AffyXell & LG Chem) & diagnostics. And as an indication of upside potential, Seattle Genetics - a US based antibody and ADC (antibody-drug conjugates) group - has a Mrkcap of $25bn. Equivalent to a 13x EV/revs multiple.

Likewise, Stifel have a 155p/share risk-adjusted valuation for the stock, which I suspect would be materially lifted in the event of future positive AVA6000 news.